When tax season rolls around, one of the most important documents for US taxpayers is the IRS 1040 form. If you’ve ever wondered “what is the IRS 1040 form?”, you’re not alone. This form is the key to filing your individual tax return, calculating your tax liabilities, and claiming any tax credits or tax deductions you’re eligible for.

In this article, we’ll break down the essentials of Form 1040, its components, and some associated schedules like 1040 schedule 1 and IRS schedule D. Whether you're filing your taxes for the first time or looking for clarity on your tax obligations, this guide will help you understand what Form 1040 entails and how to file it correctly.

Introduction to the 1040 form

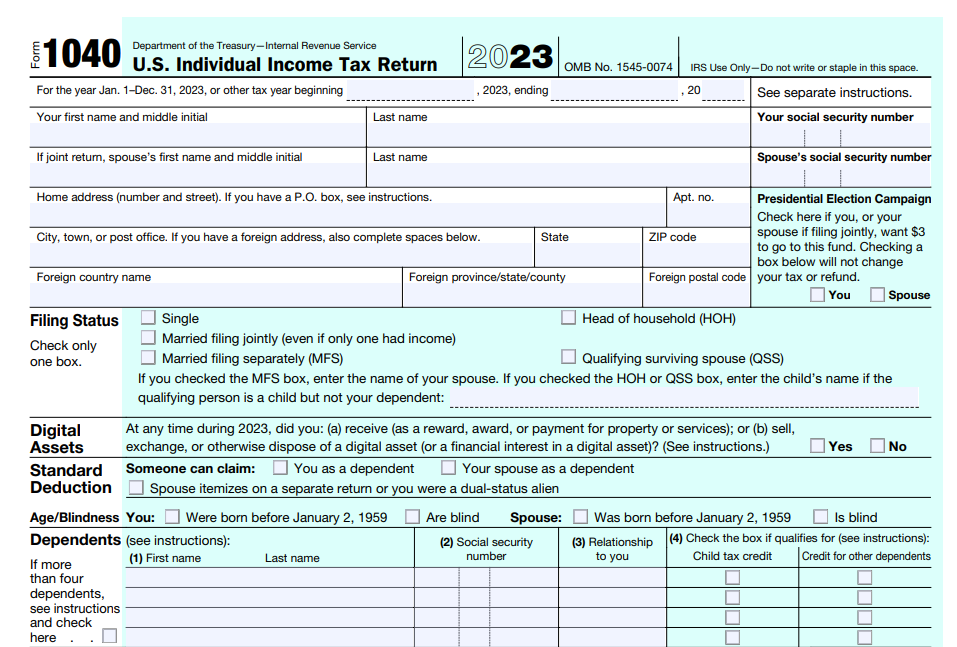

What is form 1040?

Form 1040, officially known as the "US Individual Income Tax Return," is the standard federal income tax form used to report an individual's adjusted gross income, taxable income, tax deductions, and credits, and to determine whether additional taxes are owed or a tax refund is due.

Unlike the previous 1040EZ or 1040A forms, which were phased out in 2018, the IRS 1040 form is now used by all US taxpayers. The form accommodates various types of income, including wages, salaries, dividends, and capital gains, among others.

Importance of form 1040 in tax filing

Filing Form 1040 is mandatory for anyone who earns above a certain threshold of income, including self-employed individuals, business owners, and investors. It not only calculates your tax liability but also allows you to claim tax deductions and credits, which can reduce your overall tax bill. The accurate completion of this form is crucial, as errors can lead to penalties or delays in receiving refunds.

Moreover, Form 1040 serves as a central document in tax filing, providing the IRS with a comprehensive snapshot of a taxpayer’s financial activities. Whether you're reporting wages from a job, rental income from properties, or gains from the sale of investments, this form compiles it all. Additionally, Form 1040 allows you to claim certain tax credits and adjustments to income, which can significantly reduce your tax burden.

Components of form 1040

Form 1040 is divided into several sections, each playing a specific role in calculating your tax obligations. Understanding these components will make the filing process smoother and reduce the chance of making errors that could delay processing or lead to penalties.

Basic information section

At the top of Form 1040, you’ll enter personal details, including your name, Social Security number, and filing status (single, married filing jointly, etc.). This section also asks for the number of dependents, which can influence your taxable income and potential deductions.

Your filing status is an important consideration as it determines your standard deduction amount and the tax brackets that apply to your income. For example, taxpayers who file as "Head of Household" may qualify for a higher standard deduction compared to those who file as "Single."

Income section

This section outlines the various types of income you earned during the tax year, such as wages, salaries, interest, dividends, and other types of income. Each type of income has its own line, ensuring that all earnings are appropriately accounted for.

In addition to wages from employment, this section covers additional income sources, such as:

- Dividends from investments

- Interest on savings accounts or bonds

- Rental income from property

- Capital gains from the sale of assets

By reporting all sources of income, you ensure that your adjusted gross income (AGI) is accurately calculated. This figure forms the basis for determining many tax benefits, such as eligibility for certain credits or tax deductions.

Deductions and credits section

Here’s where you can claim itemised deductions or the standard deduction. These reduce your adjusted gross income, potentially lowering your taxable income. You’ll also enter any eligible tax credits, which can directly reduce the taxes you owe.

Tax credits are particularly valuable because they provide a dollar-for-dollar reduction in the amount of tax you owe. Some common credits include the Child Tax Credit, Earned Income Tax Credit, and the Education Credits.

Additionally, taxpayers must decide between taking the standard deduction or itemised deductions. While the standard deduction is simpler and faster, itemising can provide greater tax savings in cases where you have significant deductible expenses, such as:

- Mortgage interest payments

- Charitable contributions

- State and local taxes (SALT)

Tax and payments section

This final section determines how much tax you owe or the refund you’re entitled to. Based on your tax brackets and the total tax you've already paid throughout the year, either through withholding or estimated tax payments, the form calculates whether you owe additional taxes or can expect a refund.

The calculation also accounts for any payments you’ve already made during the year, such as income tax withholding from your paycheck or estimated tax payments made quarterly by self-employed individuals.

Common schedules associated with form 1040

Many taxpayers need to file additional forms, or tax schedules, alongside Form 1040, depending on their financial situation. Let’s explore two of the most commonly used schedules:

Schedule 1 (additional income and adjustments to income)

What is schedule 1?

Form 1040 Schedule 1 is used to report income that isn’t included on the main 1040 form, such as unemployment compensation, rental income, or prize money. It also includes adjustments to income, such as student loan interest, self-employed retirement contributions, and the educator expense deduction.

Schedule 1 plays a critical role in ensuring that all types of additional income are captured. Some income types, such as gambling winnings or business income from a side gig, are often overlooked but are still taxable.

Common entries in schedule 1

- Unemployment compensation

- Rental and royalty income

- Business income

- Adjustments for self-employed health insurance

By filling out form 1040 schedule 1, you ensure that your additional income and possible deductions are properly accounted for, which helps to calculate your total taxable income more accurately.

Schedule D (capital gains and losses)

What is schedule D?

If you’ve sold assets like stocks, bonds, or real estate during the tax year, you’ll need to file an IRS report of your capital gains and losses. This schedule distinguishes between short-term gains (on assets held for one year or less) and long-term gains (on assets held for more than a year), as they are taxed at different rates.

Reporting capital gains and losses

Capital gains tax can significantly affect your tax liability, especially if you’ve realised substantial gains. On the flip side, reporting capital losses can help reduce your taxable income, potentially lowering your overall tax bill.

Capital gains are reported in two categories:

- Short-term gains, which are taxed at your ordinary income tax rates.

- Long-term gains, which are typically taxed at lower rates, ranging from 0% to 20%, depending on your income level.

It’s essential to keep accurate records of all asset transactions throughout the year to ensure you report them correctly on schedule d tax form.

Other relevant schedules

Beyond Schedule 1 and Schedule D, taxpayers may also need to file other tax forms with their 1040 form. These include:

- Schedule A. for itemised deductions like medical expenses, mortgage interest, and charitable contributions.

- Schedule C. for reporting income or loss from self-employment or business operations.

- Schedule E. for reporting income from rental properties or other investments.

Frequently asked questions

What is form 1040 schedule 1? Form 1040 Schedule 1 is an additional form used to report income not included in the main 1040 form, as well as adjustments to income such as student loan interest and retirement contributions.

How to complete schedule D? To complete Schedule D, you need to report any capital gains or losses from the sale of assets, like stocks or property. Ensure that you differentiate between short-term and long-term gains, as they are taxed at different rates.

What are the penalties for incorrect filing? Filing your taxes incorrectly can result in penalties, including late fees and interest charges on unpaid taxes. Double-check all your entries and consider using tax software or consulting a professional to avoid these issues.

Tips for Accurate Tax Filing

Filing taxes can be complicated, but by following these tips, you can ensure accuracy and avoid common mistakes.

Gathering necessary documents. Before you start, collect all the documents you need, including your W-2, 1099 forms, and receipts for any tax-deductible expenses. Organising these ahead of time will make filing much smoother.

Avoiding common mistakes. Mistakes like entering incorrect Social Security numbers, failing to sign the return, or making maths errors are common. Double-check your entries to avoid delays or penalties.

Utilising tax software or professional help. For added convenience and accuracy, consider using tax software or hiring a tax professional. These services can help you ensure that all forms and schedules are completed correctly, maximising your deductions and minimising your tax liability.

That is not financial advice.

Conclusion

Filing Form 1040 is an essential part of the tax process for US taxpayers. Understanding the form’s components, such as the income, deductions, and credits sections, along with its associated schedules, like IRS schedule 1 and schedule D tax form, can make the process less intimidating. By following the tips and guidelines outlined in this article, you’ll be well-equipped to file your return accurately and on time, potentially saving yourself money and stress during tax season.

🤔 Do you believe in crypto taxes? Share your views in our socials!

💌 Telegram, Twitter, Instagram, Facebook

Here are three other cool articles:

Understanding protocols: the backbone of digital communication

3 years with legal Bitcoin — how El Salvador has changed

What is leverage trading? A comprehensive guide

This article is not investment advice or a recommendation to purchase any specific product or service. The financial transactions mentioned in the article are not a guide to action. It’s not intended to constitute a comprehensive statement of all possible risks. You should independently conduct an analysis on the basis of which it will be possible to draw conclusions and make decisions about making any operations with cryptocurrency.